Mortgage Refinance

Understanding How Switching Lenders Can Save You Money.

Refinancing a home loan means switching your existing mortgage from one bank to another, typically to secure a lower interest rate and reduce overall interest costs. It can also be done to access additional funds through a cash-out refinancing, where you borrow against the increased value of your property.

It’s important to distinguish refinancing from repricing.

Why refinance your home loan?

Why refinance your home loan?

What Happens After Your Promotional Rate Ends?

Just like how many people re-contract their mobile plans every 1–2 years, most homeowners in Singapore refinance their mortgages on a similar cycle. Home loans often come with a promotional rate during the lock-in period, but once that period ends, the rate typically increases—usually by around 0.5%.

For example, on a $1 million loan, this rate hike could cost you an extra $5,000 a year in interest. If you’re on a fixed rate, your mortgage will automatically switch to a higher, non-promotional floating rate once the term ends—potentially increasing your monthly repayments significantly.

Refinancing at the right time can help you avoid these added costs.

Why Not Just Reprice with the Same Bank?

Repricing means switching to a different interest rate package within your current bank. While it may seem more convenient, it usually comes with a fee of around $800 to $1,000. More importantly, the packages offered to existing customers are often less competitive—or at best, similar—to those offered to new customers.

On the other hand, refinancing involves moving your loan to another bank, which typically offers more attractive rates and subsidies to offset legal and valuation costs. These incentives make switching more cost-effective in the long run.

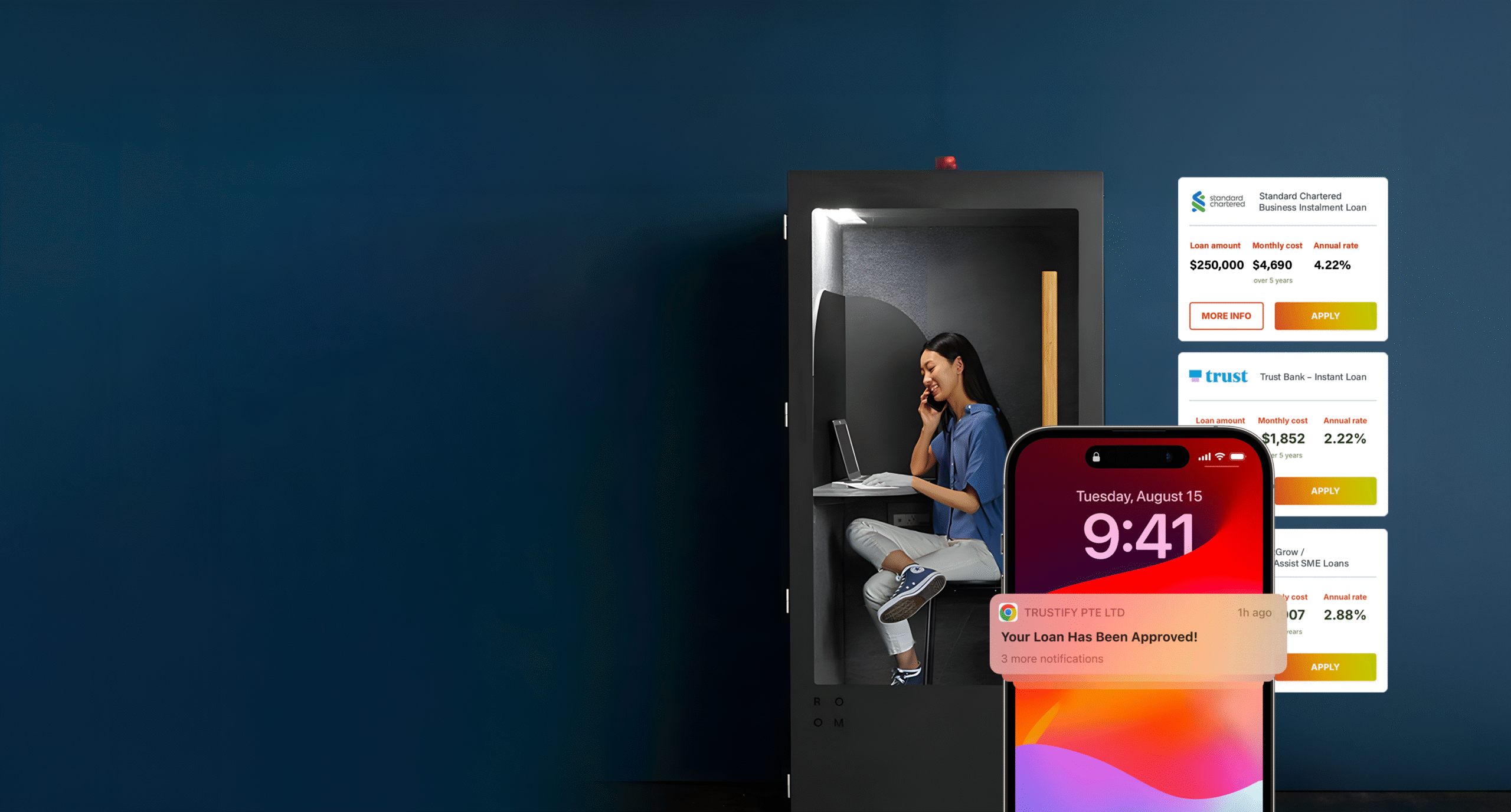

If you’re eligible for these subsidies, refinancing is usually the smarter financial move. And when you refinance through Trustify, you’ll also receive additional cashback—just like how telcos reward you for porting over your number.

Key Differences in Refinancing for HDB and Private Homes

If you choose to refinance from an HDB concessionary loan to a bank loan, the decision is irreversible—you will no longer be able to switch back to an HDB loan in the future.

In the current high-interest environment, HDB loans remain attractive, offering a stable concessionary rate of 2.6% (CPF Ordinary Account rate + 0.1%). In contrast, bank loan rates are currently upwards of 3.7%.

However, in a low interest rate environment—such as between 2009 and 2019—bank loan rates were often lower than the HDB concessionary rate, making them a more cost-effective option during that period.

| Private Property | HDBs |

|---|---|

| Eligible as private properties can only be financed by banks | You can refinance from an HDB concessionary loan to a bank loan. However, you cannot refinance a bank loan to an HDB concessionary loan. |

| Bank to bank refinancing is eligible |

When Is the Best Time to Refinance Your Home Loan?

Refinancing your home loan should be a well-timed, strategic decision. Most banks require a 3-month notice period before you can switch to another lender, so it’s important to know when your lock-in period ends. To avoid paying a penalty for early termination, you should start planning and exploring your refinancing options at least 4 months in advance.

While refinancing during the lock-in period is possible, it usually comes with a penalty fee—so timing matters.

Not sure when your current loan contract ends? Just contact your bank’s mortgage hotline, or let us at Trustify assist you in checking your loan details.

Explore Mortgage Loan Solutions From Our Trusted Lending Partners.

After you’ve explored the three key mortgage options—equity, new homes, and refinancing—it’s time to put your affordability to the test. Simply key in a few details, and you’ll discover the maximum value of the property you can afford.

Understand Your Mortgage

Mortgage Loan

Let’s work on your project together