The Ultimate Guide to Financing Your New Home in Singapore

From HDB flats to luxury private properties, this comprehensive guide walks you through everything you need to know about securing the right property loan in Singapore.

Understand Your Mortgage

Mortgage Loan

Explore Mortgage Loan Solutions From Our Trusted Lending Partners.

After you’ve explored the three key mortgage options—equity, new homes, and refinancing—it’s time to put your affordability to the test. Simply key in a few details, and you’ll discover the maximum value of the property you can afford.

Affordability assessment

Mortgage Servicing Ratio (MSR)

Affordability assessment

MSR

MSR limits the portion of your monthly gross income that can go toward mortgage repayments for HDB and executive condominiums. Capped at 30%, it ensures responsible borrowing—for example, with a $4,000 income, your mortgage repayment cannot exceed $1,200. This safeguard helps keep your home purchase within manageable means.

Total Debt Servicing Ratio (TDSR)

Affordability assessment

TDSR

Unlike MSR, which applies only to HDB and EC purchases, the Total Debt Servicing Ratio (TDSR) applies to all property types, including private homes. It limits your total monthly debt obligations—including mortgages, car loans, credit card bills, and personal loans—to no more than 55% of your gross monthly income. TDSR helps ensure that borrowers maintain healthy debt levels across all financial commitments.

Loan-to-Value (LTV) Ratio

Affordability assessment

LTV

The LTV ratio defines how much you can borrow relative to your property’s value, acting as a safeguard against over-leveraging.

- For HDB Concessionary Loans (applicable to BTO, SBF, ROF, and resale flats), the maximum LTV is 90% of the lower of the property value or purchase price.

- For bank loans, the maximum LTV is 75%—if you have no existing home loan. Of the remaining 25%, at least 5% must be paid in cash, while the remaining 20% can be covered by cash or CPF Ordinary Account (OA) savings.

HDB Flats Guide

HDB

Concessionary loan

HDB Concessionary Loan

HDB offers eligible buyers a housing loan at a concessionary interest rate, pegged at 0.1% above the CPF Ordinary Account interest rate, currently at 2.60% p.a. While this rate may be higher than some bank loans (especially floating rate packages), the key advantage is a higher Loan-to-Value (LTV) ratio of up to 90%, significantly reducing the upfront cash needed for your downpayment.

HDB

HLE eligibility

HDB Loan Eligibility (HLE) Letter

To apply for an HDB loan, you must first obtain an HLE letter, which confirms your eligibility and outlines the maximum loan amount, estimated monthly installments, and repayment terms.

Key details:

- Validity: 6 months from the date of issue

- Requirements: Assessed based on age, income, and financial position

- When to apply:

- BTO purchase: Required before flat booking

- Resale purchase: Required before exercising the Option to Purchase (OTP)

HDB

HLE application

How to Apply for an HLE

- Apply via the HDB e-Service portal using your SingPass

- Submit required documents in PDF or JPG format (max 5MB each)

- Application is valid for 30 days in draft form

- Once fully submitted, HDB processes your application within 14 working days

- You can track your application on My HDBPage > My Flat > Application Status > HLE

HDB

Other Option

What If You’re Not Eligible for an HDB Loan?

If you don’t meet the criteria for a concessionary HDB loan, your only alternative is a bank loan. However, this requires a higher downpayment of 25%, with 5% in cash and the remaining 20% via CPF-OA or cash.

Resale Private Properties Guide

Resale

Fixed Rate

Fixed Rate

A fixed interest rate ensures that your home loan rate remains unchanged for a period of 2 to 5 years, depending on your bank’s lock-in terms. This means your monthly repayments stay consistent, allowing for more predictable budgeting and easier cash flow management.

Once the fixed-rate period ends, your loan may shift to a floating rate or increase based on market conditions. When this happens, it’s advisable to reprice or refinance with your bank to secure a more competitive rate.

Resale

Floating Rate

Floating Rate

Floating interest rates are variable rates that fluctuate based on market conditions. In Singapore, they typically come in two forms:

- Board Rates – set internally by individual banks

- SORA Rates – pegged to the Singapore Overnight Rate Average, published daily by the Monetary Authority of Singapore (MAS)

The most widely used benchmark is the 3-month compounded SORA rate. While floating rates may offer lower initial interest, they are subject to changes over time, which can affect your monthly repayments. This option may suit buyers who expect interest rates to fall and are comfortable with some level of risk.

New Launch Private Property (BUC)

BUC

Fixed Rate

Fixed Rate

A fixed interest rate keeps your home loan rate unchanged for a period of 2 to 5 years, depending on your bank’s lock-in terms. This ensures consistent monthly repayments, which helps with budgeting and cash flow management.

After the lock-in period, your loan may shift to a floating rate or increase based on market conditions. When this happens, consider repricing or refinancing with your bank to secure more favorable terms.

BUC

Floating Rate

Floating Rate

Floating rates are variable and can change based on market trends. In Singapore, they typically come in two forms:

- Board Rates – set internally by banks

- SORA Rates – based on the Singapore Overnight Rate Average, published daily by the Monetary Authority of Singapore (MAS)

The most common reference is the 3-month compounded SORA rate. While floating rates may offer lower initial interest, they carry the risk of rising over time—making them more suitable for borrowers comfortable with fluctuations in their monthly payments.

Progressive Payment Scheme (PPS)

Before Monthly Loan Repayments

Stage 1

Secure the Option to Purchase (OTP)

To begin, you’ll need to pay a 5% booking fee in cash to secure the Option to Purchase (OTP). Once the OTP is issued, the developer is required to deliver the Sale & Purchase Agreement (S&PA) within 14 days.

Exercise the OTP and Sign the S&PA

You must exercise the OTP within 3 weeks of receiving the S&PA. If you decide not to proceed, 25% of the booking fee will be forfeited, while the remaining 75% will be refunded within 4 weeks.

📘 Tip: Learn more about the process in our guide – “5 Steps Before Exercising the OTP”

Make the Downpayment & Pay Stamp Duties

Upon signing the S&PA, you are required to pay an additional 15% downpayment within 8 weeks from the OTP date. This can be paid via cash or CPF Ordinary Account (OA).

At this point, you will have covered:

- 5% booking fee

- 15% downpayment

- Total: 20% of the purchase price

You can now proceed to secure a 75% bank loan and settle any applicable stamp duties, including:

- Buyer’s Stamp Duty (BSD)

- Additional Buyer’s Stamp Duty (ABSD) (if applicable)

After Monthly Loan Repayments

Stage 2

Progressive Payment Schedule (PPS) for Buildings Under Construction (BUC)

Once your loan transitions into the Building Under Construction (BUC) phase, funds from your approved home loan are disbursed progressively based on the construction milestones.

As each stage is completed, your loan amount increases accordingly, and so do your monthly repayments. These payments start off lower and gradually rise in tandem with the disbursement schedule.

Why Do You Need an Approved BUC Loan Now?

Consideration

Why Do You Need an Approved BUC Loan Now?

You might be wondering why it’s necessary to get a Building Under Construction (BUC) loan approved now, especially when the actual disbursement happens progressively. Here are three key reasons:

- Access to CPF Funds

An approved BUC loan is required to tap into your CPF Ordinary Account to pay the remaining downpayment beyond the initial 5% booking fee. - Future-Proofing Your Eligibility

Securing loan approval now protects you from potential changes in your financial status—such as job loss or reduced income—that could affect your ability to qualify for a loan later. - Lock in Attractive Interest Rates

Promotional or low variable rates may not last. If you’re satisfied with the current loan packages, getting approval now allows you to lock in these rates before they change.

What Types of Loan Packages Are Available for BUC?

Consideration

What Types of Loan Packages Are Available for BUC?

BUC loans are typically offered as variable rate packages and are committed to the full approved loan amount. For example, if you’ve secured a loan of S$1 million, the bank is contractually obligated to disburse the full amount progressively according to the Progressive Payment Scheme (PPS)—as long as you continue to meet your monthly repayment obligations on time.

Key Features to Consider in BUC Loans

🔁 Conversion Options

Most BUC loans offer conversion flexibility, allowing you to switch to newer promotional or fixed-rate packages—especially after the Temporary Occupation Permit (TOP) is issued.

This is valuable because promotional rates typically last for the first 3 years, after which they revert to higher standard rates. If your property hasn’t reached completion by then and you’re not eligible to refinance, converting to a more favorable package helps lower your interest costs.

Most banks offer up to two free conversions over the loan tenure.

🔓 No Lock-in Period

BUC loans generally come with no lock-in period, giving you the freedom to make partial or full repayments at any time without incurring early repayment penalties.

❌ Cancellation Fees

If you cancel your BUC loan before full disbursement, banks typically charge a cancellation fee ranging from 0.75% to 1.5% of the undisbursed loan amount—regardless of property type.

🏗️ Disbursement After TOP

Upon issuance of the Temporary Occupation Permit (TOP), 25% of the purchase price is disbursed. The remaining 15% is released in stages based on whether the Certificate of Statutory Completion (CSC) or property title is issued first:

If title is issued before CSC: 2% → 8% → 5%

If CSC is issued before title: 8% → 5% → 2%

Let’s work on your project together

How do I apply for a home loan?

Our consultation is always in sync with your strategy

Yes, you can.

Simply let us know your preferences by emailing us at Info@trustifysg.com or informing us during our follow-up call after you’ve submitted your application.

Restricted lenders will not be able to access your contact information or submitted documents.

-

✅ Access 80+ Trusted Lending Partners

Compare loan offers from top banks and licensed financial institutions in Singapore. -

⚡ Fast & Hassle-Free Approvals

Receive personalised loan offers in as little as 48 hours — no repeated paperwork. -

🔒 Secure & MAS-Compliant

Your data is safe. We work only with licensed lenders regulated by the Monetary Authority of Singapore. -

💡 Transparent & Pressure-Free

No hidden fees, no obligations — just honest comparisons and the right loan for your needs.

At Trustify, we’re on a mission to make borrowing smarter, faster, and stress-free.

Apply once. Get matched. Choose confidently.

Yes, absolutely.

At Trustify, we recognise that family offices are an emerging and valuable source of SME financing. We welcome your participation in our lending ecosystem.

By joining our network, you’ll gain access to curated business loan requests through our Business Loan Marketplace, allowing you to explore potential lending opportunities aligned with your investment criteria.

To learn more or begin the onboarding process, please reach out to us at

📩 Info@trustifysg.com or

📱 WhatsApp us at +(65) 8058 8598

At Trustify, your privacy is our top priority. Our smart matching system anonymises your personal details during the loan comparison process — sharing only what’s necessary for our lending partners to generate accurate, personalised offers.

Your contact information is never shared until you’ve selected and accepted an offer, ensuring full control over your data.

All our partners are licensed and regulated by the Monetary Authority of Singapore (MAS) and are legally bound to comply with strict data protection laws. With Trustify, you can explore your loan options safely, securely, and with confidence.

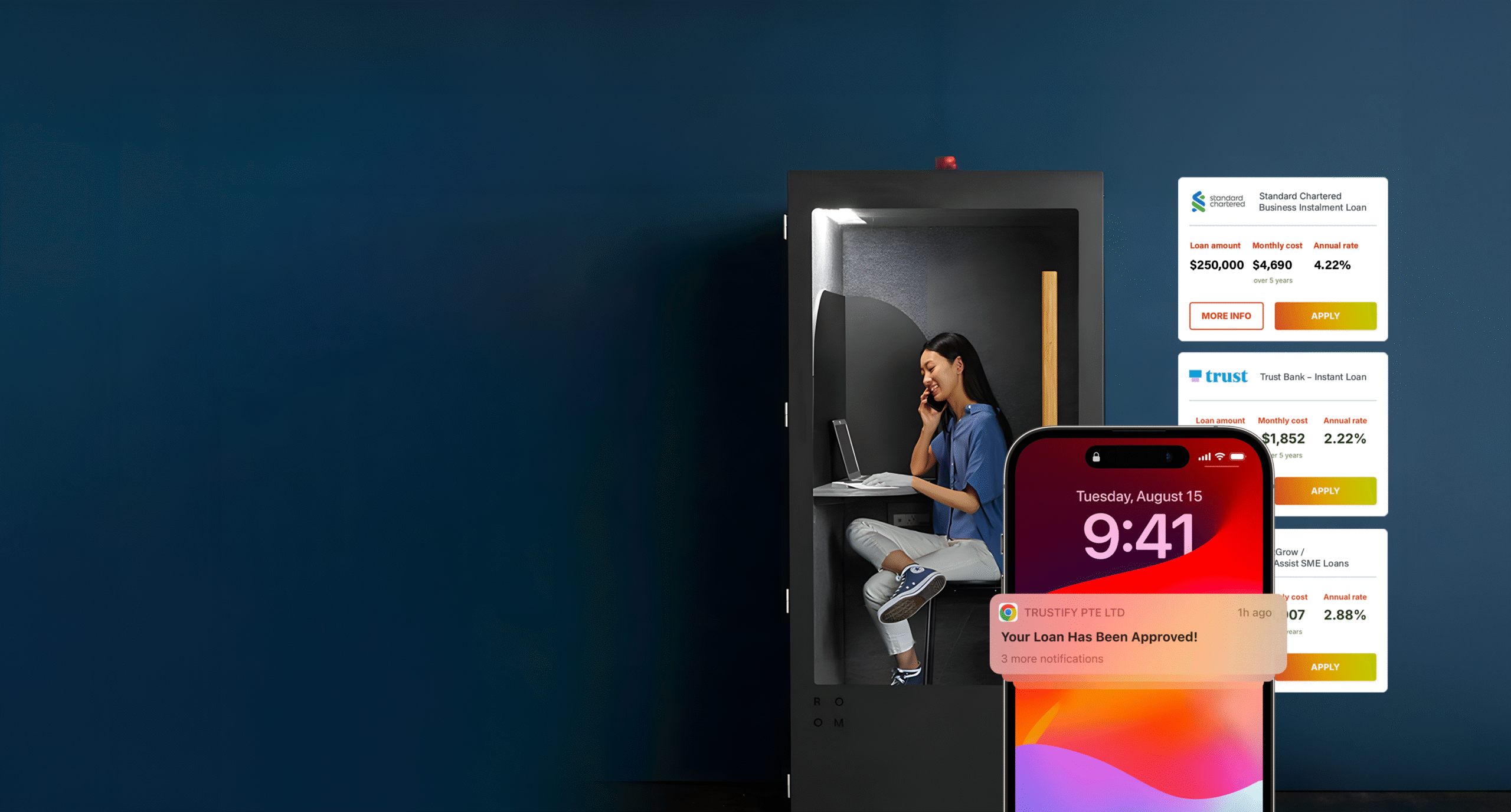

At Trustify, we work exclusively with licensed and MAS-regulated financial institutions to ensure safety, transparency, and credibility. Our panel includes some of Singapore’s leading banks — such as DBS, CIMB, and Standard Chartered — along with reputable non-bank financial providers.

With access to a wide network of over 80+ trusted lending partners, we make it easy for you to compare and secure the most suitable loan options — all through a single, secure application.

Unlike generic comparison platforms that only display advertised rates, Trustify connects you with real, personalised loan offers through a single application. We understand that advertised rates don’t reflect what you’ll actually receive — because every borrower’s financial profile is unique.

Our intelligent matching system takes your individual circumstances into account, delivering pre-qualified loan offers tailored to your needs. This gives you the clarity to choose the best loan, without the guesswork.

Plus, our dedicated customer support team is here to guide you — for free. From application to disbursement, we’re with you every step of the way to ensure a smooth, informed, and stress-free borrowing experience.

Trustify is Singapore’s trusted digital loan platform, connecting you with personalised loan offers from multiple banks and licensed financial institutions.

With just one simple online application, our intelligent matching system protects your privacy while allowing lenders to assess your profile and present customised rates — all within minutes. No more chasing quotes or comparing banks manually — Trustify brings the best loan options directly to you.