Start-up Loan

Kickstart Your Business

with a Start-Up Loan

")

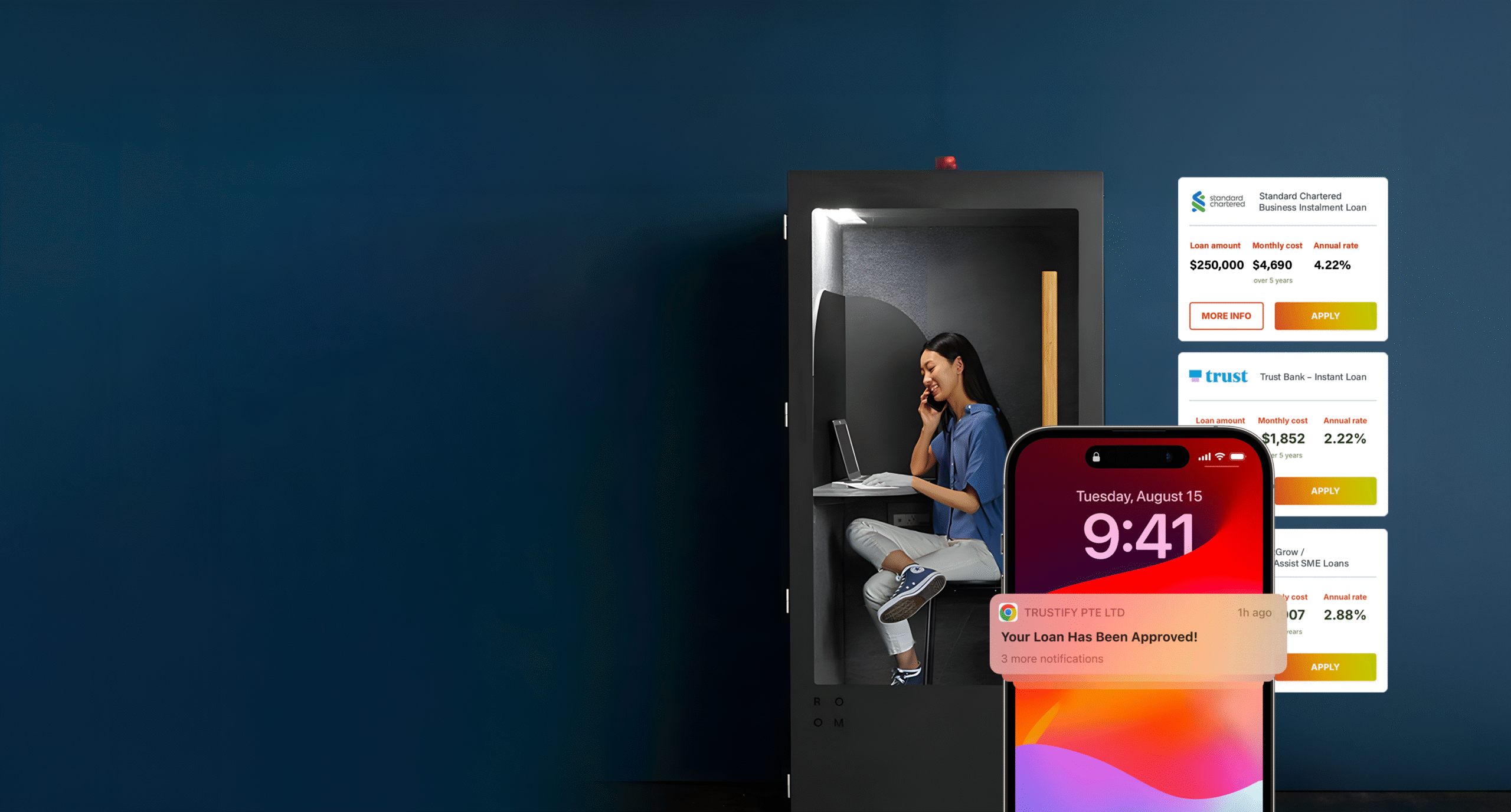

Explore Start-up Loan solutions from our trusted lending partners.

Option 1: Personal Loan

Option 2: Share-backed Loan

Option 3: Insurance-Backed Loan

Option 1: The Hidden Advantage of Using Personal Loans for Start-Ups

New businesses often face a major hurdle—lack of operating history or track record—which makes securing traditional business loans nearly impossible. And even if approved, these loans can come with steep interest rates, sometimes as high as 3–4% per month. When you crunch the numbers, a personal loan can turn out to be a more practical and cost-effective option. Here are a few reasons why.

The Standard Personal Loan

A personal loan is credited directly to the borrower’s bank account, offering full flexibility in how the funds are used. Unlike auto or renovation loans—which are disbursed directly to car dealers or contractors—personal loans are not tied to specific purchases, making them a more suitable option for business-related expenses.

Income Statement

Trustify personal loan guide

Your Income Determines Your Loan Eligibility

The loan amount you qualify for is typically a multiple of your monthly income, based on your annual earnings. Refer to the table below for an estimate.

Banks in Singapore typically cater to individuals earning over S$30,000 annually, offering loan amounts of up to 8 times their monthly income. Those earning below this threshold can only access financing through licensed money lenders.

Individuals with annual incomes between S$20,000 and S$30,000 are in a favourable position, as they can borrow up to 6 times their monthly income. Meanwhile, for those with no declared income or earning less than S$20,000 a year, the maximum loan available is capped at S$3,000.

Credit Bureau Score

Trustify personal loan guide

Check Your Credit Bureau Score

Your Credit Bureau Report is the second most important factor lenders consider when evaluating your loan application. Here’s a quick breakdown of what matters most on your report:

Key Factors That Affect Loan Eligibility:

- Overall Credit Grade

- Any History of Default or Bankruptcy

- Whether a Credit Score is Available

How to Check Your Credit Score in Singapore

You can obtain your credit report from Credit Bureau Singapore (CBS) through:

- Online Request – Receive a softcopy by email. link me there

- In-Person Request – Collect a hardcopy from any SingPost outlet, CBS office, or CrimsonLogic Service Bureau

Fees:

- S$6.42 (including GST)

- Add S$2.00 if you choose multiple delivery options

- S$17.12 administrative fee for 2-hour express collection at SingPost outlets

Interest Rate

Trustify personal loan guide

Compare Interest Rates

When it comes to borrowing, interest rates can make a big difference in your overall repayment amount. Banks generally offer more affordable rates compared to licensed money lenders.

| Lender | Interest Rate | Processing Fee |

|---|---|---|

| Banks | 6% – 8% p.a. (EIR) | ~1.5% |

| Licensed Money Lenders | 1% – 4% per month (up to 48% p.a.) | 2.5% – 7% |

Note: Interest rates from money lenders are capped by the Monetary Authority of Singapore (MAS).

Understanding Interest Rates in Singapore

When reviewing loan offers, you’ll typically see two different types of rates:

Effective Interest Rate (EIR)

The EIR represents the actual cost of borrowing, as it includes not only the nominal interest rate but also any processing fees and the effects of compounding based on your repayment schedule. In Singapore, financial institutions are required to display the EIR to help borrowers make more informed comparisons.

Annual Percentage Rate (APR)

APR reflects the yearly cost of a loan, including fees and charges, but excludes compounding. While APR gives a broad sense of cost, it may not reflect the real monthly repayment burden as accurately as EIR.

Tenure

Trustify personal loan guide

Consider the Loan Tenure

Loan tenure plays a key role in determining your monthly repayment. Banks offer longer tenures—up to 5 years—making monthly instalments more manageable. In contrast, licensed money lenders typically offer shorter terms of up to 24 months. Given their higher interest rates, extending the loan beyond 2 years is usually not cost-effective.

| Lender | Maximum Loan Tenure |

|---|---|

| Banks | Up to 5 years |

| Licensed Money Lenders | Up to 24 months |

Why Option 1: Personal Loan Could Be the Right Choice for You

When it comes to personal loans, choosing between banks and licensed money lenders isn’t always straightforward. While banks are generally the preferred option due to lower interest rates and longer tenures, licensed money lenders serve a valuable role in situations where banks may not be an option. Here are three scenarios where a licensed money lender may be the better fit:

Loan-to-Value (LTV) Ratio

You can borrow up to 70% of the market value of your assets, depending on the type and stability of the security.

Example: If your stock is worth S$1,000, you may be eligible for up to S$700 in financing.

Note: If the LTV exceeds 90% due to market fluctuations, a top-up may be required.

Loan-to-Value (LTV) Ratio

Borrow up to 90% of your policy’s latest guaranteed surrender value.

The actual amount and LTV ratio depend on the type of policy and the issuing insurer.

Our services

Other Loan We Offer